Self-pay healthcare continues to be on the rise, so we can’t ignore it. As the proportion of consultants’ income from self-pay hits a new record high, we think this trend is likely to continue growth - even as we move into more certain times, post COVID pandemic.

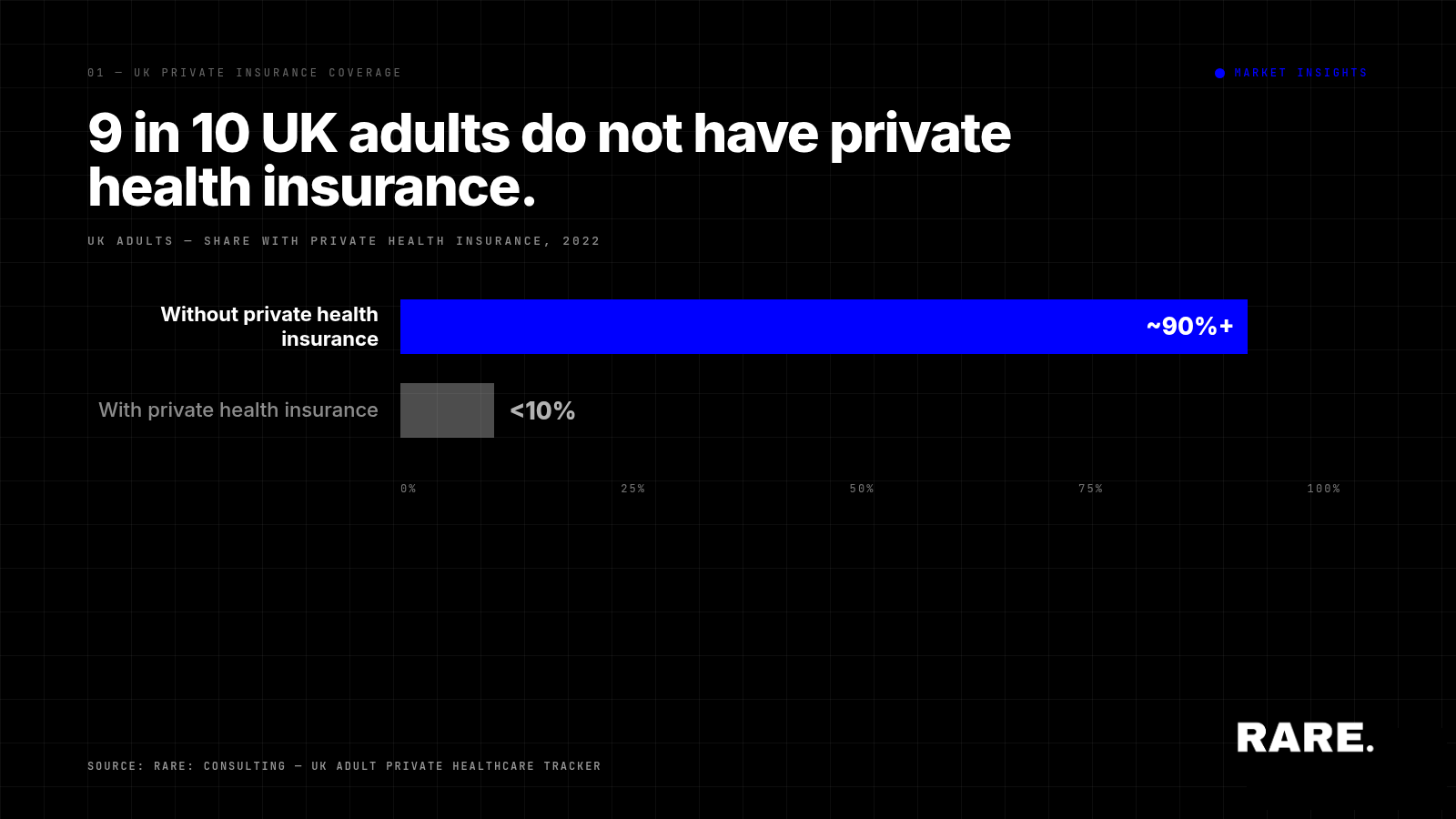

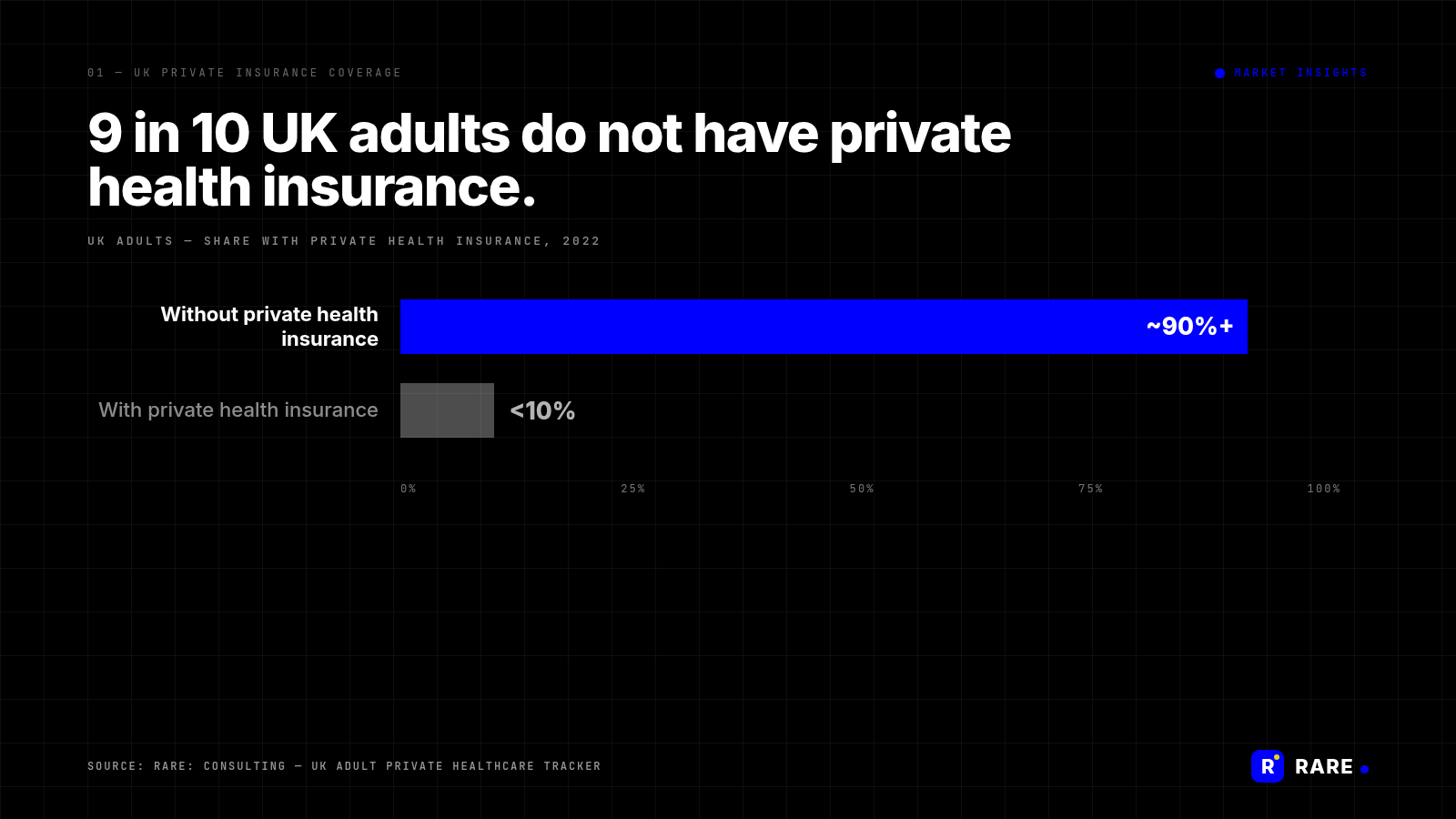

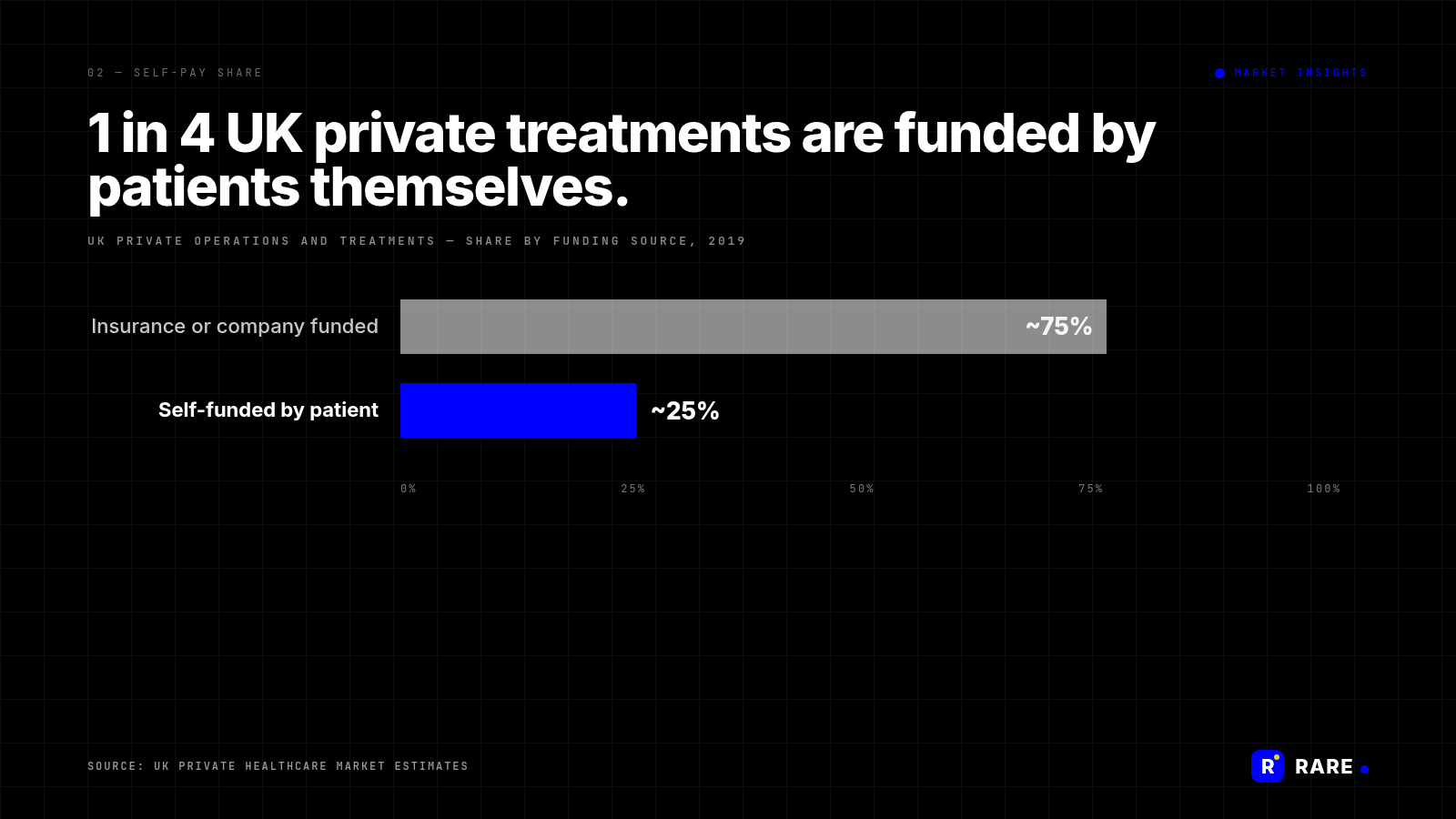

More than 90% of UK adults do not have private health insurance, yet roughly 1 in 4 UK private treatments are now patient-funded rather than insurance-funded, according to Rare. research. The rise of self-pay reflects two converging realities: NHS waiting times that are pushing UK consumers towards private alternatives, and insurance policies that increasingly carry exclusions and excesses that erode their value at the point of need. The structural shift is reshaping how UK private healthcare is funded.

How is private health insurance distributed across UK adults?

UK private healthcare has historically been understood as an insurance-led market. The reality is different. More than 90% of UK adults do not hold private health insurance.

That distribution alone makes self-pay the dominant funding mechanism for any UK private healthcare provider planning beyond the corporate insurance market. Private health insurance covers a small minority of the UK adult population, and many of those policies now carry escalating excesses, exclusions and pre-existing condition restrictions that limit their practical value at the point of treatment.

How much UK private healthcare is now self-funded?

Even back in 2019, before the pandemic accelerated the trend, around 200,000 UK private operations and treatments per year, roughly 1 in 4, were patient-funded rather than insurance- or company-funded.

The 1-in-4 share has continued to grow in subsequent years. The proportion of consultants reporting income from self-pay has hit successive record highs. The trajectory has continued through the cost-of-living pressure that began in 2022, suggesting that the demand driver is structural NHS pressure rather than discretionary consumer spending.

What is driving UK consumers towards self-pay healthcare?

The single dominant driver is immediacy. UK consumers do not generally choose self-pay because they believe the treatment or practitioner will be better than the NHS. They choose self-pay because they want to be seen sooner. NHS waiting times of 18 weeks and longer for elective treatments make immediacy a far more valuable proposition than perceived treatment quality.

The treatment areas with the highest current and historic self-pay activity reflect this. UK private dental and optical services, both of which have been substantially privatised for decades, lead the rankings. Physiotherapy and mental health services follow, both areas where NHS underfunding and waiting times have been most pronounced.

What barriers still hold self-pay back?

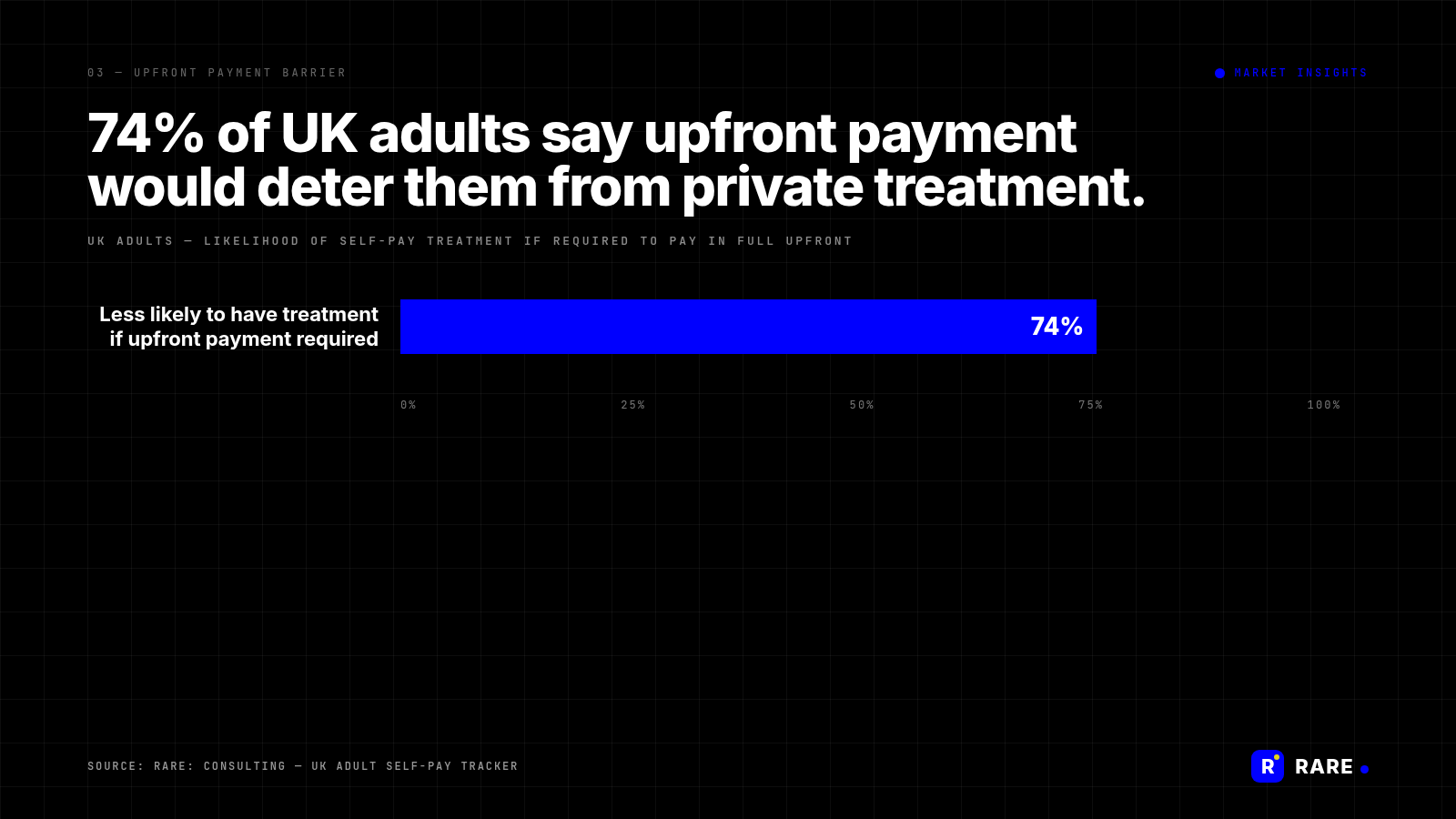

Cost remains the primary barrier to wider self-pay uptake. 74% of UK adults say that having to pay in full upfront would make them less likely to have private treatment.

This is the clearest commercial gap in the UK self-pay market. Providers that solve the upfront-payment friction through financing, instalment plans and transparent total-cost models will absorb meaningful demand from consumers who otherwise stay on NHS waiting lists. The gap also widens the socio-economic divide if it is left unaddressed: only those who can pay upfront access timely treatment, while those who cannot remain on long NHS lists. Financing models help close that gap.

The 74% number is the most useful figure in this analysis. It tells you the size of the UK self-pay market the upfront-payment model is actively keeping out. Three-quarters of UK adults who would consider private treatment if they could pay over time are not converting because they are being asked to find several thousand pounds in advance. This is not a price problem. It is a financing infrastructure problem. The providers that solve it will not redistribute share among themselves. They will expand the size of the UK self-pay market. That is a different commercial proposition from the one most UK private hospitals are currently running on.