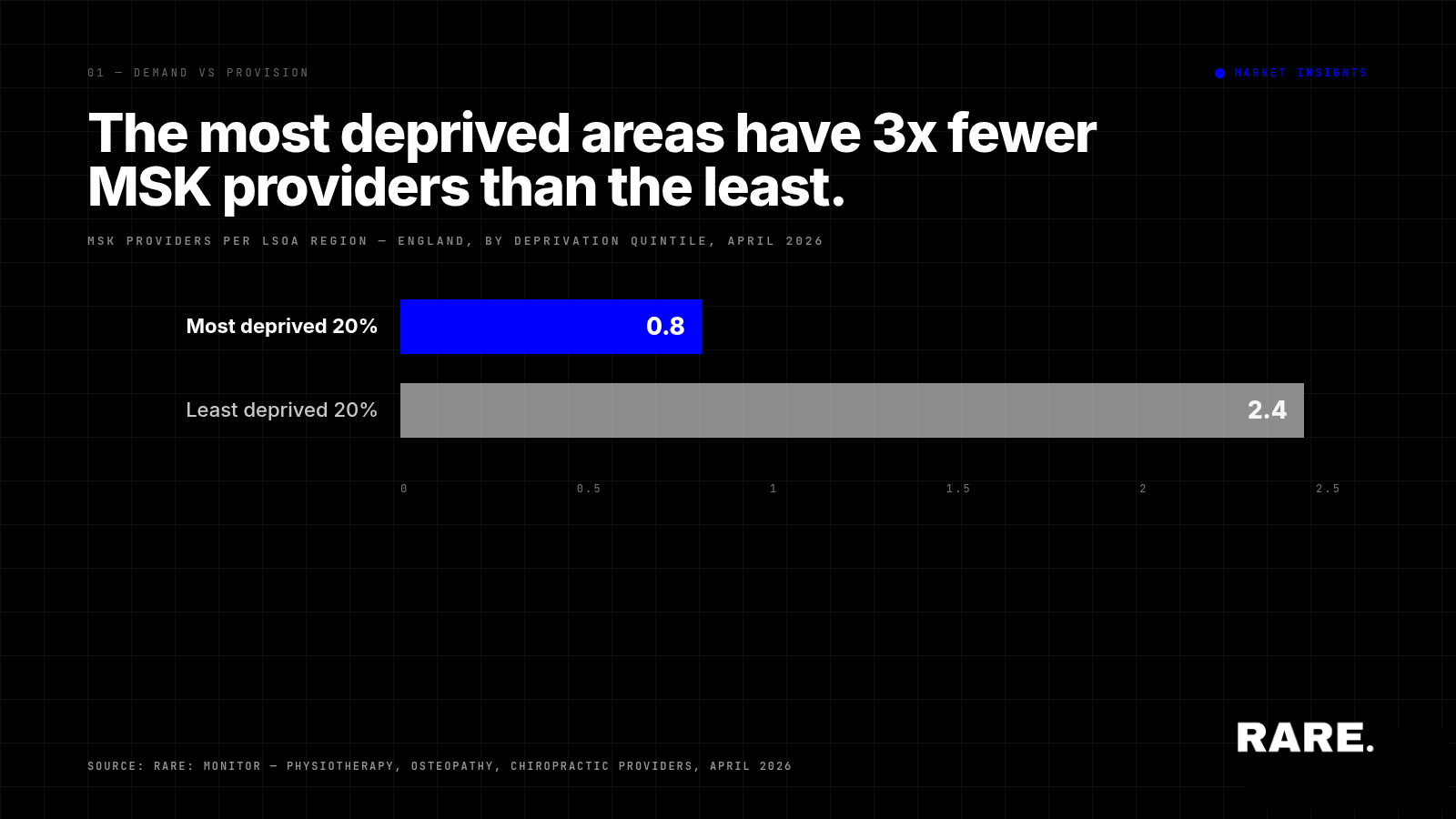

In the most deprived areas of England, one in four GP patients reports an MSK condition, yet these areas have three times fewer physiotherapy, osteopathy, and chiropractic providers than affluent regions. This analysis maps exactly where the unmet demand sits across every Sub-ICB, and what it means for manufacturers, service providers, and commissioners targeting the MSK market.

The UK musculoskeletal (MSK) market covers physiotherapy, osteopathy, and chiropractic services. At the time of writing this article (April 2026), Rare.Monitor tracks over 16,000 physiotherapy clinics, 10,000 osteopathy practices, and 2,700 chiropractic clinics across the country. This analysis maps the gap between clinical need and provider access across every Sub-ICB in England, and identifies the areas where unmet demand is highest.

In the most deprived areas, around one in four GP patients reports arthritis or a musculoskeletal condition. Yet these same areas have roughly three times fewer MSK providers than affluent regions. The more deprived the area, the higher the clinical need, and the fewer the providers. For manufacturers, service providers, and commissioners, that mismatch represents the largest concentration of unmet demand in the market.

If you sell into the MSK market, this is where your next set of customers are.

Where is MSK demand highest in England?

Arthritis, back, and joint problems are not evenly distributed. Our analysis shows areas with higher levels of deprivation consistently see higher rates of these conditions among their GP populations.

This pattern holds across every deprivation group, from the most deprived to the least. Each estimate is drawn from hundreds of GP practices, so the averages are stable and reliable. The more deprived the area, the greater the MSK burden on local communities.

For manufacturers and service providers, this is a map of underserved demand. The communities carrying the greatest MSK burden are also the ones with the fewest options. That creates a clear opportunity for those who can reach them.

How are physiotherapy, osteopathy, and chiropractic services distributed?

Our analysis maps provision against need for every Sub-ICB in England. The areas with the highest arthritis rates have the fewest healthcare providers. Conversely, the areas with the lowest need are over-served.

Market forces, and historic commissioning decisions, have pushed services towards areas where patients are more likely to self-fund. The communities that should be prioritised are the ones being overlooked. Provider data from the Chartered Society of Physiotherapy, the General Osteopathic Council, and the General Chiropractic Council confirms how heavily concentrated private provision remains in affluent postcodes.

How wide is the gap between MSK need and provider access?

The most deprived areas report an estimated arthritis rate of around 25% among GP patients, yet have fewer than 0.8 MSK providers per LSOA region. The least deprived areas have the lowest arthritis rates but roughly three times more providers.

The areas with highest clinical demand are the areas with fewest providers. For anyone selling into the MSK market, that is where the growth is.

Why are providers missing the biggest MSK opportunity?

Affluent clustering. Private providers cluster in affluent areas. It is a move for short-term stability: targeting patients who can self-fund or who rely on private health insurance. But it leaves the bigger market untouched.

Untapped opportunity. The country's most deprived regions have the highest clinical need and the least provision. Both the NHS and the private sector are leaving patients behind. For those willing to go where others aren't, the opportunity is potentially substantial.

The regulatory bodies overseeing these professions, including the Health and Care Professions Council for physiotherapy and the Institute of Osteopathy, have highlighted the need for broader geographic access to musculoskeletal care. The data supports their position.

Where MSK demand is highest, supply is thinnest

The structural pattern in the data is that physiotherapy, osteopathy and chiropractic provision concentrates in lower-need, higher-income regions. The areas with the highest deprivation-driven MSK burden, often the same areas with high concentrations of physical-labour industries, have the fewest providers per head. The NHS does not compensate.

The contracted-pathway routes (ICB commissioning, employer-funded provision, PCN partnerships) are the established mechanisms for bridging that supply gap, and the data above shows where the gap is widest. Providers and manufacturers willing to operate in those underserved catchments will reach a more urgent need than those concentrating in already-served areas.

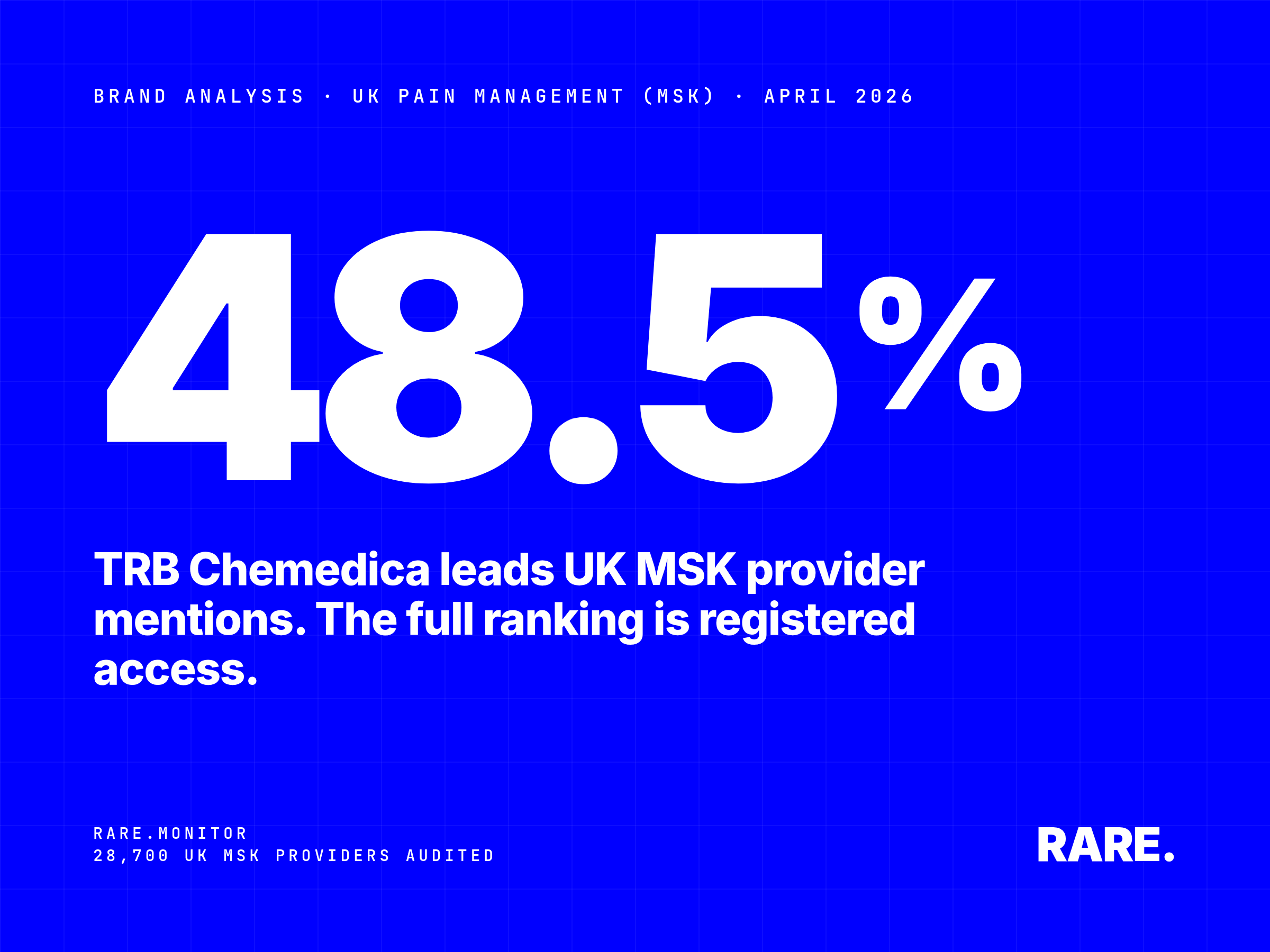

For a breakdown of which pain management brands are gaining traction across UK MSK providers, see our companion report: Brand Amplification in Pain Management.