Earlier this month, we were invited to take part in the first ever MAIS conference, put together by the esteemed Dr Benjamin Ascher.

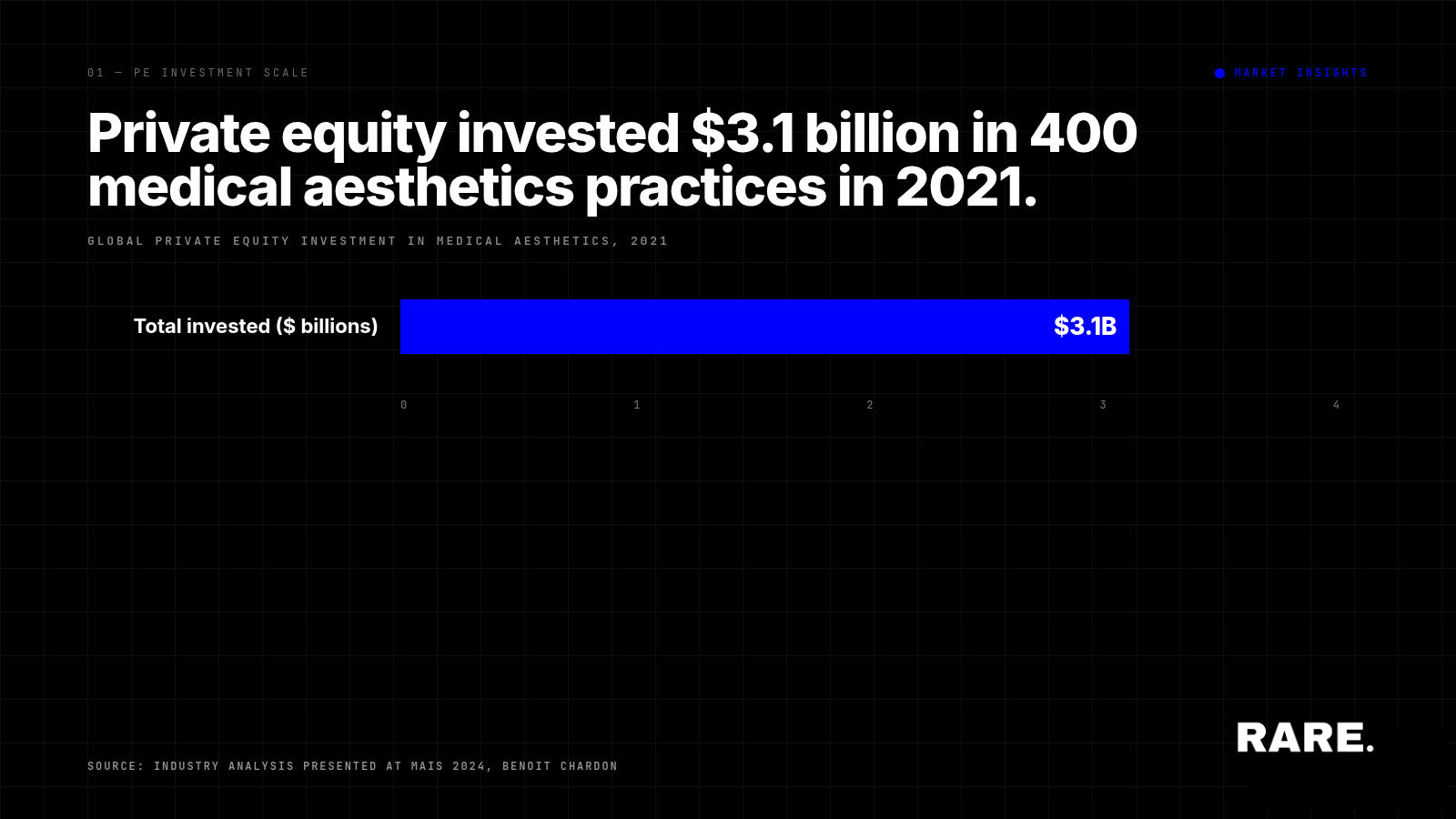

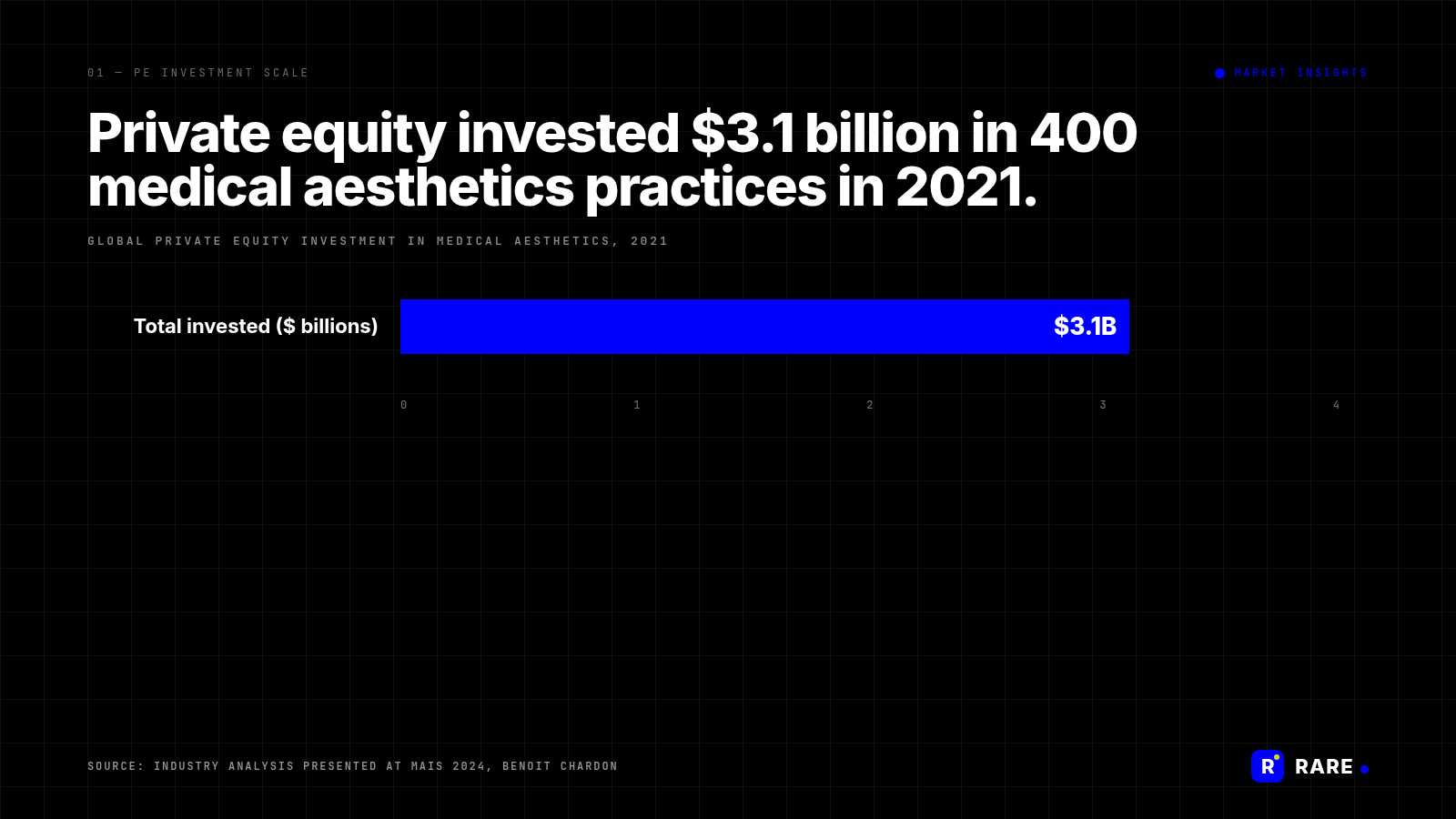

Private equity invested $3.1 billion across 400 medical aesthetics practices in 2021 alone, according to industry analysis presented at MAIS 2024 by Benoit Chardon. The figure has continued to grow since. PE-backed consolidation is reshaping clinical practices, patient experiences and competitive structure across global medical aesthetics, and the discussion at MAIS 2024 captured both what makes that pattern work and where it goes wrong.

Why does private equity in medical aesthetics succeed in some hands and fail in others?

The MAIS panel was unusually candid about failure modes. Domonic Mazzone, drawing on his work in medical aesthetic data, identified unsustainable growth as the dominant cause of PE-backed clinic bankruptcies: rapid location expansion without long-term planning, poor operational management, and a lack of patient-centred approaches. Tracy Cohen Sayag, CEO of Clinique des Champs Elysées, made the same point from the operating side: patient care has to remain at the forefront, otherwise clinics lose patients to poor experience faster than new patients can be acquired through marketing.

The successful PE-backed clinics, by the same panel, share three operating habits: they prioritise patient satisfaction, they invest in technology, and they retain skilled clinical talent. Clinics that try to substitute aggressive marketing for any of those three almost always struggle long-term.

What metrics matter for PE-backed medical aesthetic clinics?

Ben Pask, founder of Rare., set out the metrics PE firms typically assess when evaluating aesthetic practice acquisitions: Place (the local market opportunity), Product (the service proposition), Patient (key customer loyalty metrics), People (clinical and operational talent retention), and Performance (overall business performance). The 5Ps framework is what PE buyers use as a diligence shape, and existing clinics can use the same framework to understand which dimensions of their business will be examined when they enter sale conversations.

Where is global PE activity concentrated?

Beyond the United States, Europe, Brazil, India and Australia all show meaningful PE activity in medical aesthetics. Larger clinic chains are emerging through PE-led acquisition of smaller practices, with operational standardisation following acquisition. The efficiency benefits are real, but so is the question raised by industry observers: what role remains for the independent practitioner-led clinic in a market increasingly defined by chain economics?

Tracy Cohen Sayag highlighted AI integration as the next operational lever, with her own group implementing AI-driven patient experience and clinic operations tooling that has measurably lifted retention. The combination of PE capital, chain operating models and AI-driven efficiency is the structural pattern most likely to define the next five years of medical aesthetics globally. Independent clinics that build their commercial models around the patient relationships PE-led chains struggle to replicate, rather than competing on scale they cannot match, are best positioned to coexist with that consolidation.

MAIS 2024 was put together by Dr Benjamin Ascher and is recommended for anyone making strategic decisions in the global medical aesthetics market. The conference brought together leading commercial decision makers and clinical innovators in the global facial injectable market, and the depth of the panel discussions reflected that calibre of audience.

Source: MAIS 2024 conference proceedings; industry analysis from Benoit Chardon, Domonic Mazzone, Tracy Cohen Sayag, Dr Karamveer S Chhabra and Ben Pask.