Bridgepoint has added the leading UK medical-grade skincare brand to a portfolio that already includes Vivacy injectables, referencing these partnerships as a way to grow in the market. But there may be a headwind ahead. Rare. Monitor’s UK clinic data shows the cross-sell affinity sits closer with energy-based devices, rather than injectables.

Bridgepoint has agreed to acquire Obagi Medical from Waldencast for up to $460 million, adding the most-named UK clinical skincare brand to a portfolio that already includes Laboratoires Vivacy, the French injectables business. Both Bridgepoint and incoming Obagi CEO Michel Brousset have publicly framed the deal as a play on the intersection of skincare and aesthetics, with named Vivacy synergies in scope. Data from 34,000 medical aesthetics clinics in the UK indicates that historically, devices may be a better category for developing cross sell synergies.

Source: Beauty Independent, June 2026; Rare. Monitor, May 2026.

The deal in brief

Bridgepoint has agreed to acquire Obagi Medical from Waldencast for up to $460 million: $366 million in cash at close, $30 million in vendor notes, and up to $64 million in earnouts tied to 2026 to 2027 revenue milestones. Headline multiples are 2.8x on 2025 net sales of $161.6 million and 23.7x on adjusted EBITDA of $19.4 million. Around two-thirds of Obagi’s revenue currently sits in the United States, with the rest spread across the Middle East, Asia and Europe.

The portfolio context matters. Bridgepoint already owns Laboratoires Vivacy, the hyaluronic acid injectables business founded in 2007 and exporting to over 85 countries (Stylage dermal fillers, Desirial intimate gels, HA viscosupplements). Brousset has been explicit that Obagi will work on synergies with Vivacy, and that Obagi will benefit from access to technologies developed by other Bridgepoint portfolio companies, "particularly Laboratoires Vivacy". Obagi itself launched its first HA dermal filler, Saypha MagIQ, in Q1 2026.

In short: an investor with an injectables franchise has just bought the leading UK clinical skincare brand, and has named the injectables franchise as the source of operational and technology synergy.

The conventional investor case

When an investor pairs injectables and medical-grade skincare in the same portfolio, the cross-sell hypothesis writes itself. Aesthetic clinics that already perform injectable procedures (botulinum toxin, dermal fillers, polynucleotides) have the prescriber relationships, the in-chair time, and the consultation moment to layer medical-grade skincare alongside the core procedure. The injectables franchise becomes the wedge; the skincare line follows. The more injectables clinics in the brand’s existing or addressable estate, the easier the cross-sell.

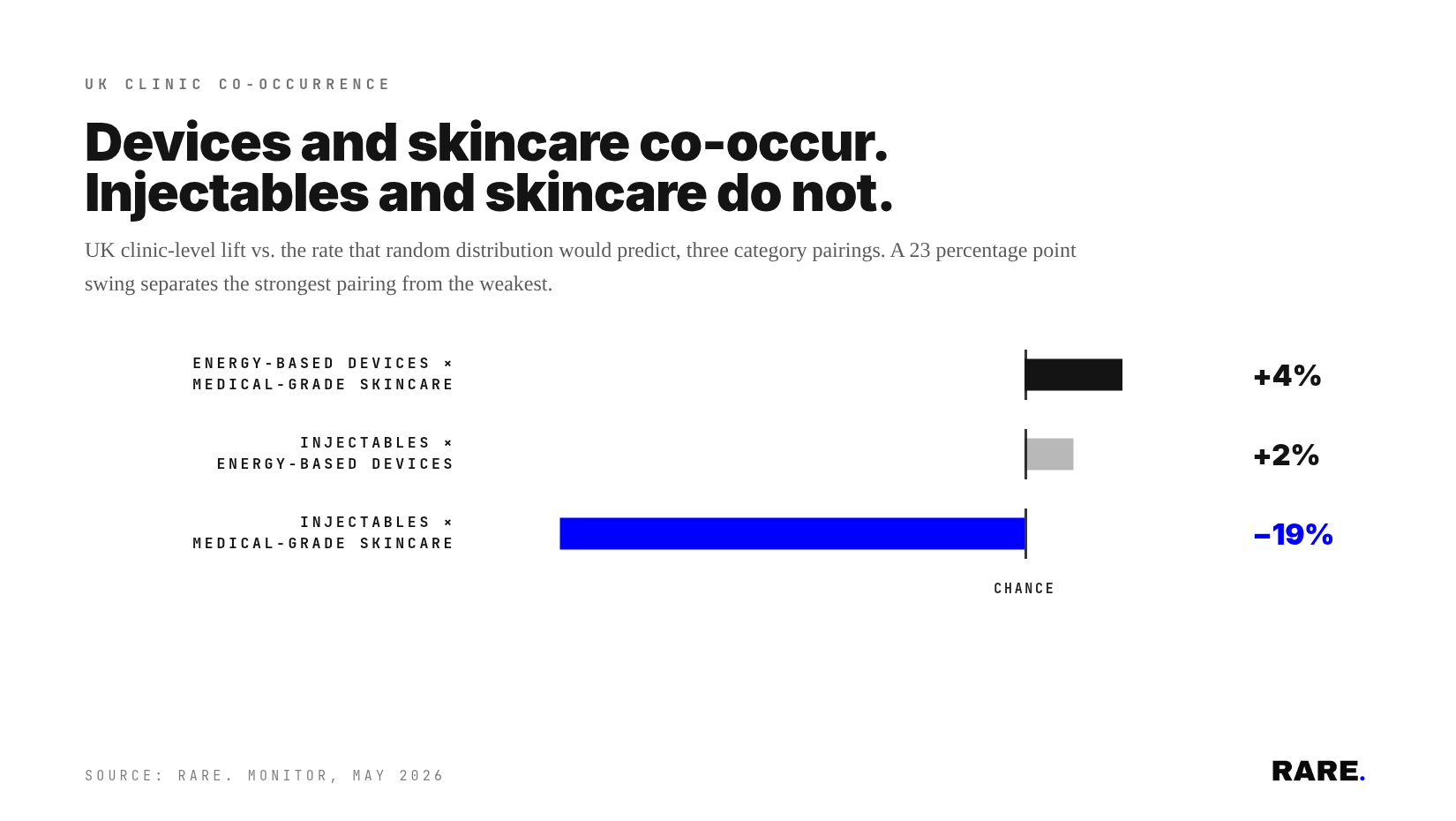

What UK clinic data actually shows

Historically, this cross-sell hypothesis has shown a different pattern. Across UK clinics tracked at the time of writing, the strongest co-occurrence between aesthetics categories is between energy-based devices and medical-grade skincare, not between injectables and medical-grade skincare.

Set against what UK clinic distribution would predict by chance:

The asymmetry sits in the third row of the chart. Injectables and medical-grade skincare are 19% less likely to share a UK clinic than UK clinic distribution would predict at random. The devices-and-skincare pairing is 4% above chance, modestly positive. That is a 23 percentage point swing between the two pairings, with devices ahead of injectables on the same measure.

In plain terms: a UK clinic offering energy-based devices is materially more likely to also stock medical-grade skincare than a UK clinic offering injectables is. The injectables-led cross-sell is the weakest of the three pairings on this metric, by some distance.

The pattern has a clinical reading. Device modalities act on the skin barrier and require a structured at-home regimen to hold the result; sunscreen, retinoids and barrier-repair products sit inside the treatment protocol, not adjacent to it. The injectables encounter does not have the same requirement, which is the most parsimonious explanation for why the cross-sell affinity sits where it does.

(The full UK clinical skincare brand leaderboard, which puts Obagi on 44.7% of the 5,088 UK clinics that disclose a clinical skincare brand, sits in our UK Medical-Grade Skincare brand analysis, May 2026.)

What this changes for the Obagi / Vivacy commercial plan

Obagi already leads the UK ranking on share-of-mentions, so the brand is not absent from the injectables-heavy estate. The point is that the next unit of UK distribution growth is unlikely to come from there. The estate where the affinity holds, energy-based device clinics, is a meaningful and growing slice of the UK aesthetics market in its own right, with multi-year capital-equipment cycles that lock the clinic into the modality once it commits.

For Bridgepoint’s UK aesthetics portfolio post-deal, three concrete implications:

The Vivacy to Obagi synergy at the technology layer is one thing. The same synergy at the UK clinic-distribution layer is a different thing, and the affinity data does not support carrying it via the injectables base.

Sales coverage for Obagi in the UK should be mapped to the device-clinic estate as a first priority, not to the Vivacy-style injectables-clinic estate. The two overlap, but the share-of-skincare affinity is not the same in each.

The growth case for layering medical-grade skincare into an injectables-only clinic depends on that clinic moving into devices, not on the injectables relationship itself. Device adoption is the better leading signal of skincare receptivity, in this dataset.

The bottom line

The case for the deal is not that Bridgepoint has bought a brand it can ride into the Vivacy injectables base. It is that Bridgepoint has bought the most-named UK clinical skincare brand at the point where energy-based devices, not injectables, are the category it natively co-distributes with. The portfolio plan that respects that asymmetry, by routing UK distribution through the device-clinic estate first and treating injectables clinics as a secondary channel, is likely to outperform one that prioritises injectables.

Methodology: This article references Rare. Monitor’s UK medical-grade skincare audit (May 2026: 14,511 UK clinics tracked; 5,088 disclosing a clinical skincare brand) and Rare. Monitor’s wider UK aesthetics provider tracking (n=34,168 providers). Co-occurrence figures are expressed as lift relative to the chance rate that UK clinic distribution would predict if the two categories were independent. A pairing 19% below chance is one that occurs 19% less often than independence would predict; a pairing 4% above chance is 4% more often. Deal facts sourced from publicly reported coverage of the Bridgepoint Group acquisition of Obagi Medical from Waldencast, announced June 2026 (Beauty Independent; Bridgepoint Group). Source: Rare. Monitor, May 2026.