Earlier this month we spoke remotely at CCR Conference, If you couldn’t attend live, don’t worry—you can watch the full session recording below.

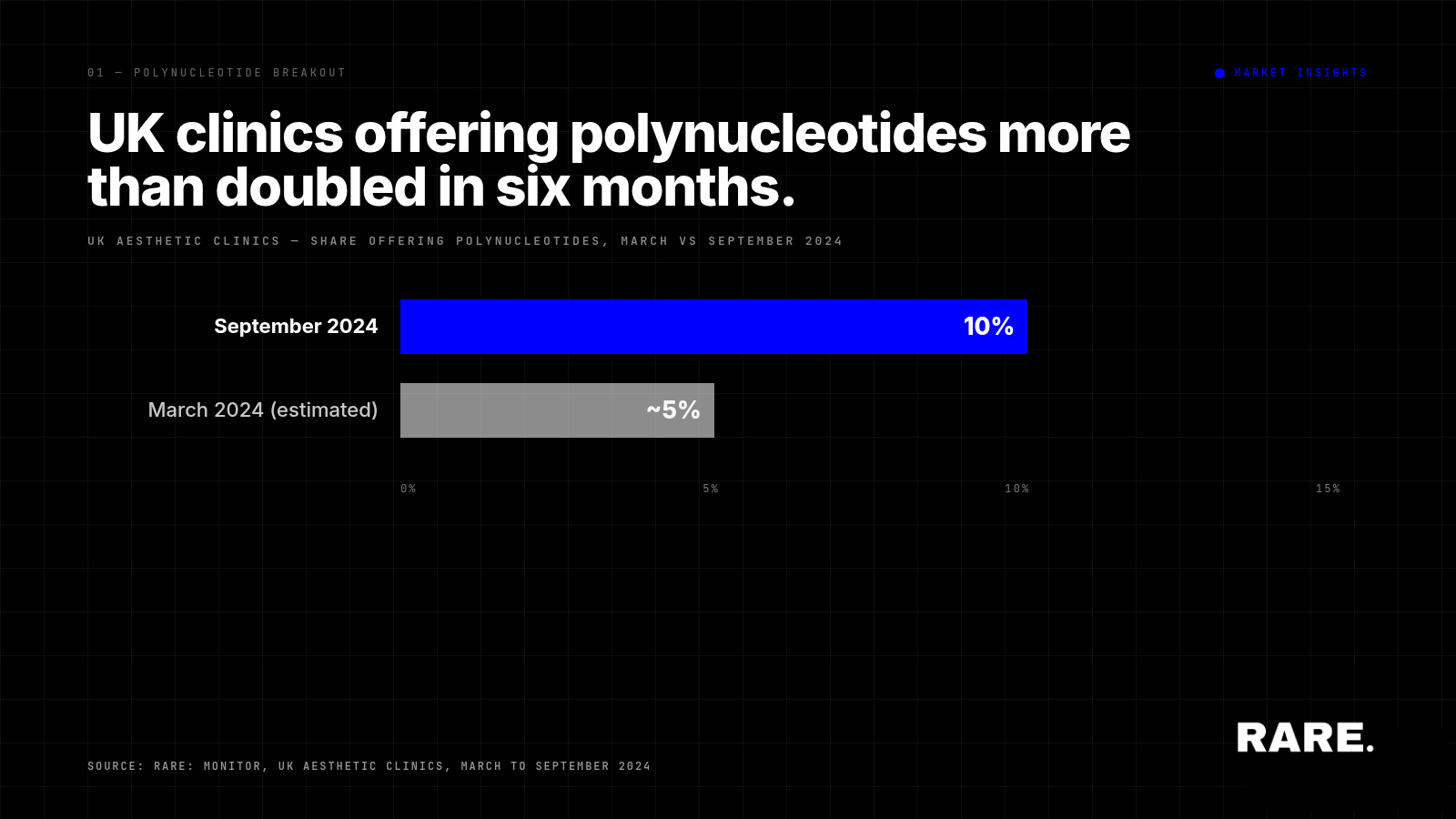

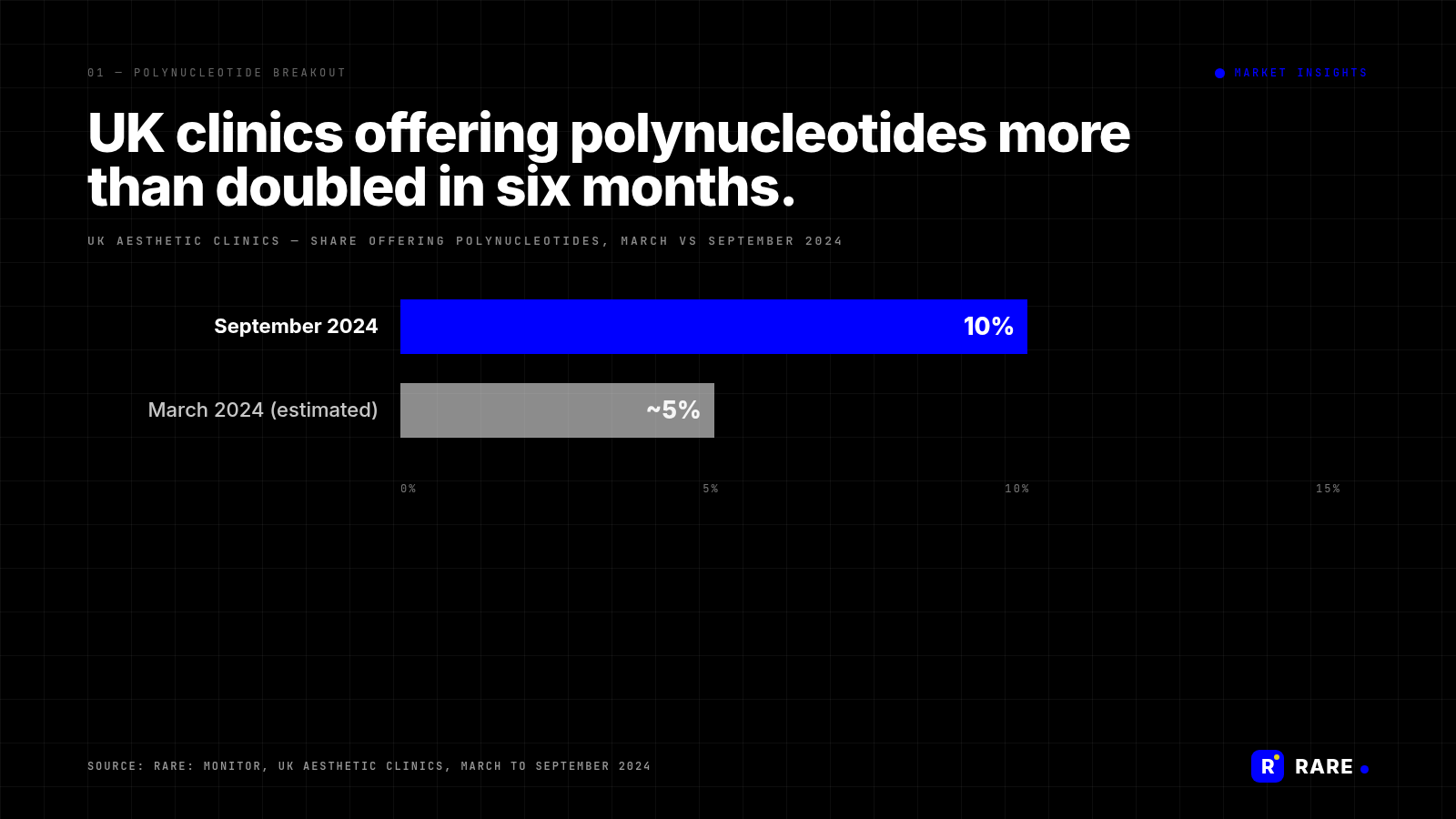

UK clinics offering polynucleotides more than doubled in six months, reaching 10% provider penetration by September 2024, according to Rare.Monitor data drawn from over 90,000 UK health, beauty and wellness providers. The polynucleotide breakout is the headline finding from the broader CCR 2024 trend analysis, but it sits alongside a wider category reset across UK aesthetics: medical wellness and longevity treatments now hold third spot among most-offered categories, and provider supply for traditional injectables is expanding even as consumer demand for them falls.

Which UK aesthetic treatment categories are growing fastest?

Polynucleotides lead category-level growth at 102% over six months, reaching 10% market penetration. Biostimulators, skin boosters, fat-dissolving treatments, and wellness and longevity treatments are all in the growing tier. Dermal fillers are an interesting outlier: provider supply is still expanding, but consumer interest is contracting. The combination compresses margins for clinics that offer dermal filler as a primary positioning rather than as one element in a broader portfolio.

Are aesthetic clinics broadening their treatment mix?

Yes, and faster than the headline category data suggests. The average UK aesthetic clinic now offers more than eight treatment types. The structural shift towards holistic wellness inside the clinic environment is visible in service-mix breadth, not just category-level adoption. UK aesthetic clinics are no longer single-treatment specialists. They are multi-treatment portfolios sold under a single clinical brand.

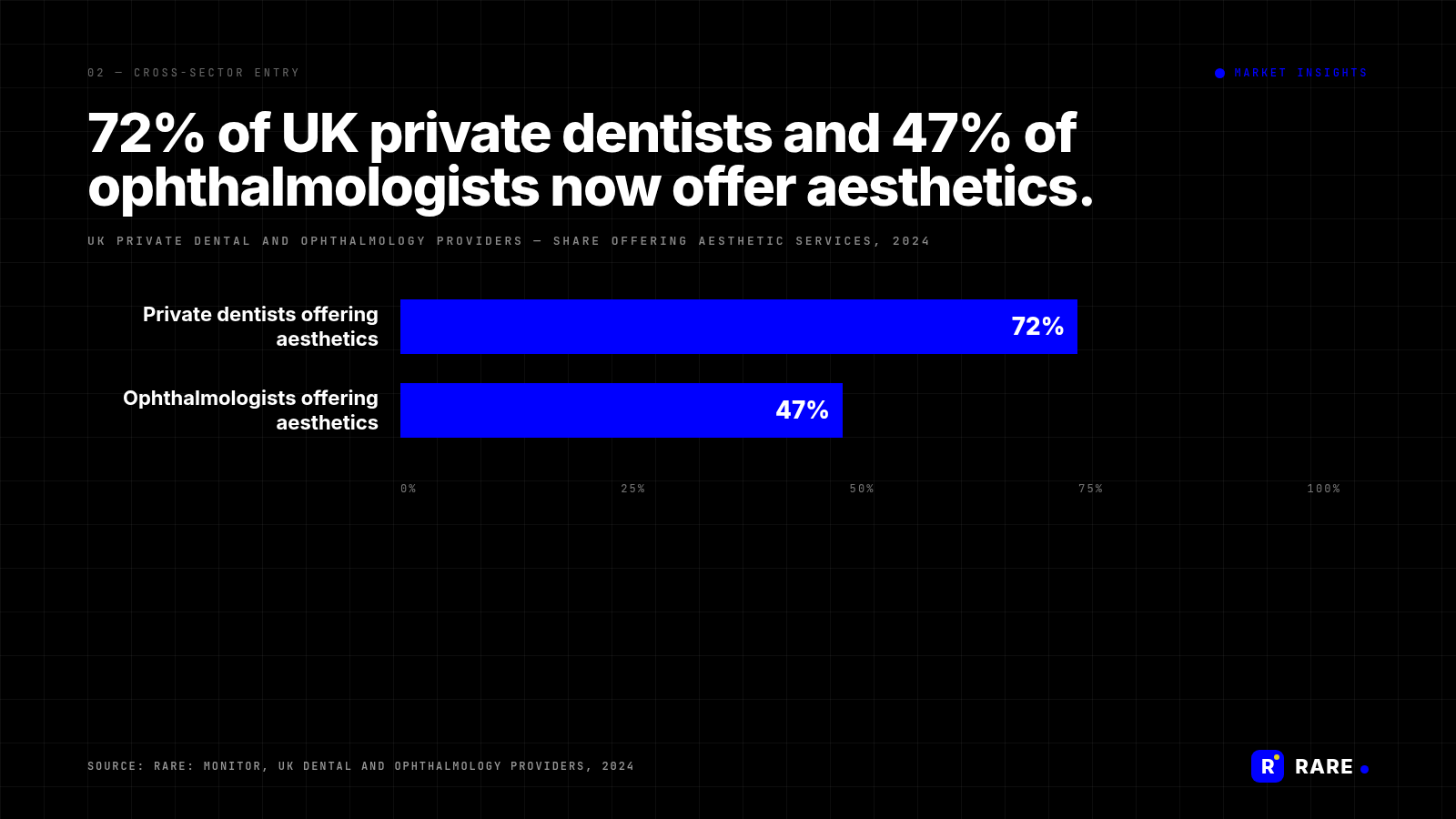

Who else is entering the UK aesthetics market?

The competitive landscape is broadening across adjacent UK healthcare sectors. 72% of UK private dentists now offer aesthetic services. 47% of ophthalmologists do.

That cross-sector entry has commercial implications most aesthetic-only providers have not fully reckoned with. The competitor set for a UK aesthetic clinic is no longer only other aesthetic clinics. It is also dental and ophthalmology practices that have added aesthetics to existing patient relationships. Both channels carry CQC registration by default and the trust signal that comes with it. Aesthetic clinics that compete on price alone, rather than on differentiated treatment portfolios or distinctive consumer brand positioning, will lose share to these adjacent entrants over time.

Polynucleotides as a category is the reverse of that pressure: a fast-growing pocket where almost no UK provider has yet established a defensible position. The clinics and brands that move into polynucleotide before the category settles will set the reference points for the wider market. Six months from now, that window will be smaller. Twelve months from now, it will be closing.

Source: Rare.Monitor, UK aesthetic providers, March to September 2024.