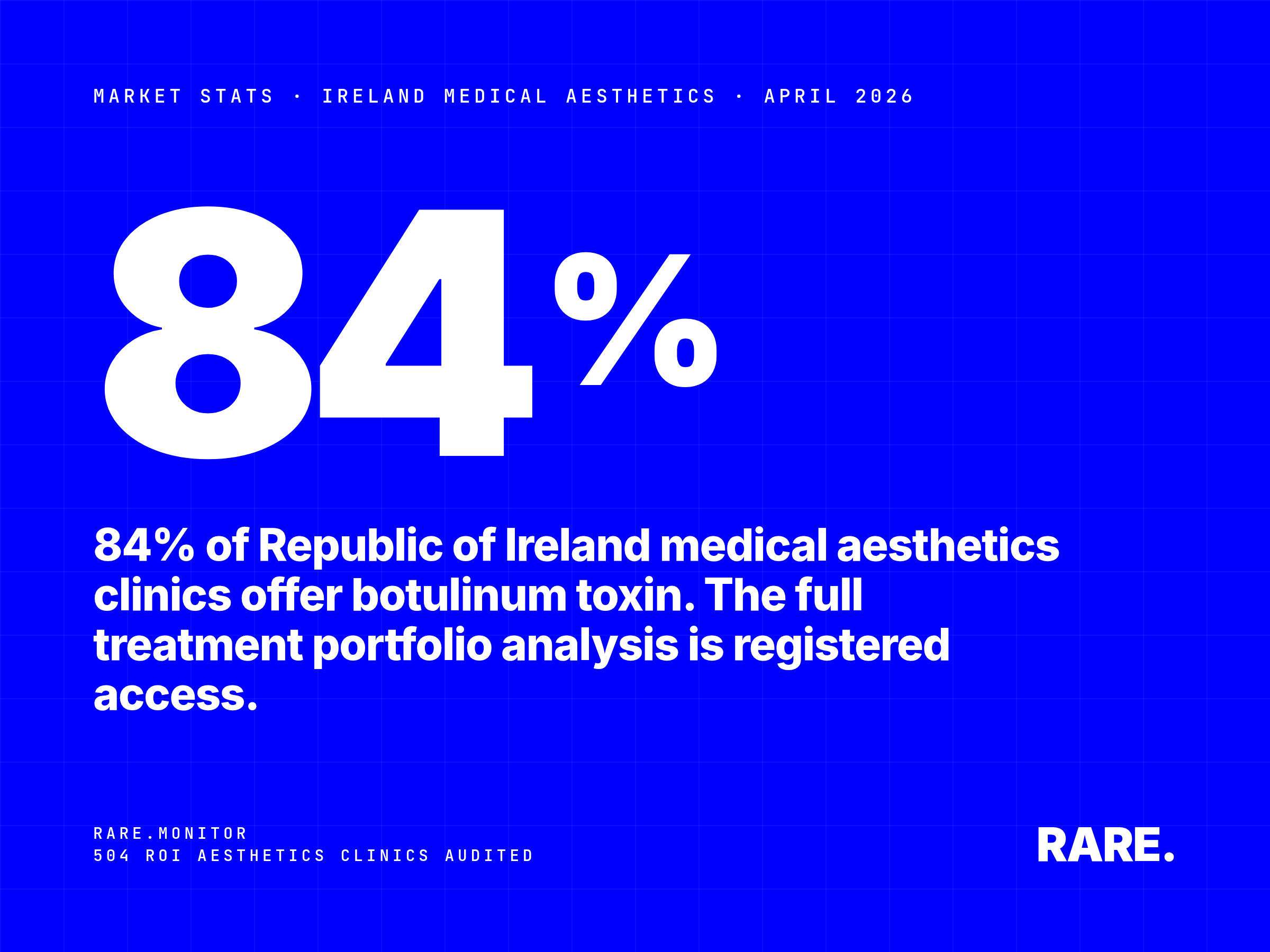

The Decline in UK Botulinum Toxin Providers: Early Impact of Impending Regulations Between September 2024 and March 2025, our data indicates a 6% decline in the number of UK clinics offering botulinum toxin treatments.

The number of UK clinics offering botulinum toxin treatments fell 6% between September 2024 and March 2025, according to Rare.Monitor data. The decline is significant, and it has happened before the new licensing framework for non-surgical cosmetic treatments has even taken effect. The market is starting to reshape itself in anticipation.

Key findings

6% decline in providers. The number of UK clinics offering botulinum toxin has fallen 6% over six months.

Regulatory compliance gap. 99% of clinics that exited the market over this period were not registered with the CQC, Healthcare Improvement Scotland, Care Inspectorate Wales, or the Regulation and Quality Improvement Authority.

Pre-emptive exit. The pattern indicates clinics that do not currently meet regulatory standards are exiting ahead of the new licensing requirements rather than going through the compliance process.

What is driving it

The UK aesthetic industry has been criticised for its lack of comprehensive regulation for years. The Joint Council for Cosmetic Practitioners and the British Association of Aesthetic Plastic Surgeons have led sustained calls for stricter oversight on patient safety grounds. The UK government's licensing framework, due to take effect in 2025, is the response.

Practitioners outside the existing CQC regulatory perimeter face a clear choice: bring the practice up to the standard required for licensing, or exit. The data suggests a substantial proportion are choosing exit. The 6% decline reflects practitioners making that calculation now rather than going through compliance later.

The other driver is legal exposure. Following several high-profile incidents involving patient harm, public and legal scrutiny of aesthetic practitioners has intensified. The combination of impending licensing and rising legal risk is the immediate cause of the contraction.

Where the market is heading

Further consolidation is the most likely outcome. Clinics already operating to high standards will absorb the patient base displaced by exits. Some providers will adapt to the new licensing requirements; others will not. The medium-term effect is a smaller, more concentrated market with higher barriers to entry.

For consumers, the consequences are mixed. Patient safety should improve as the unregulated tier exits the market. Treatment availability is likely to fall in some geographies in the short term, and prices will likely rise as the supply contracts. The trade-off, fewer providers offering safer treatment, is what the licensing framework was designed to deliver.

What this means for the rest of the market

The 6% decline is the start of a transition that will play out over the next 24 to 36 months. Manufacturers selling botulinum toxin into the UK aesthetic market need to anticipate a smaller, more institutional channel and adjust commercial planning accordingly. Field forces calibrated to the previous channel structure will be over-resourced for the new one.

99% of exiting providers were operating outside CQC, HIS, CIW, or RQIA registration. The signal that the regulatory perimeter is being enforced, even before the formal licensing date, is unambiguous. The compliance question for clinics not yet registered is no longer whether to register but when. Source: Rare.Monitor, March 2025.