COVID-19 has had an unprecedented effect on the UK healthcare system, placing a great strain on the public healthcare system. There has been a vast reduction in many procedures carried out by the NHS, and an increase in wait lists that may take years to return to normal levels. Many consumers who may not previously have used private healthcare are considering the use of self-pay healthcare, as they seek alternatives to NHS wait lists.

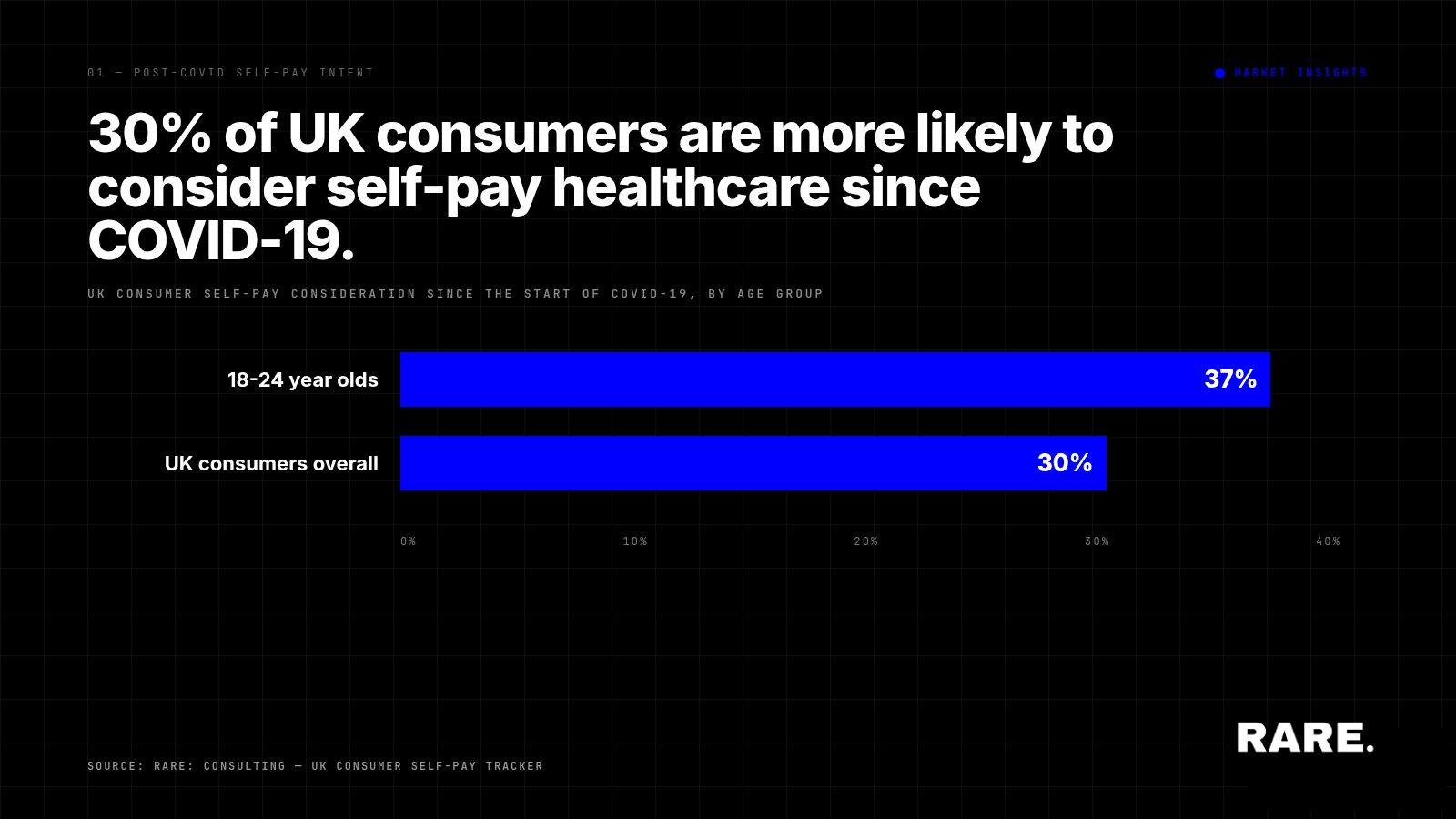

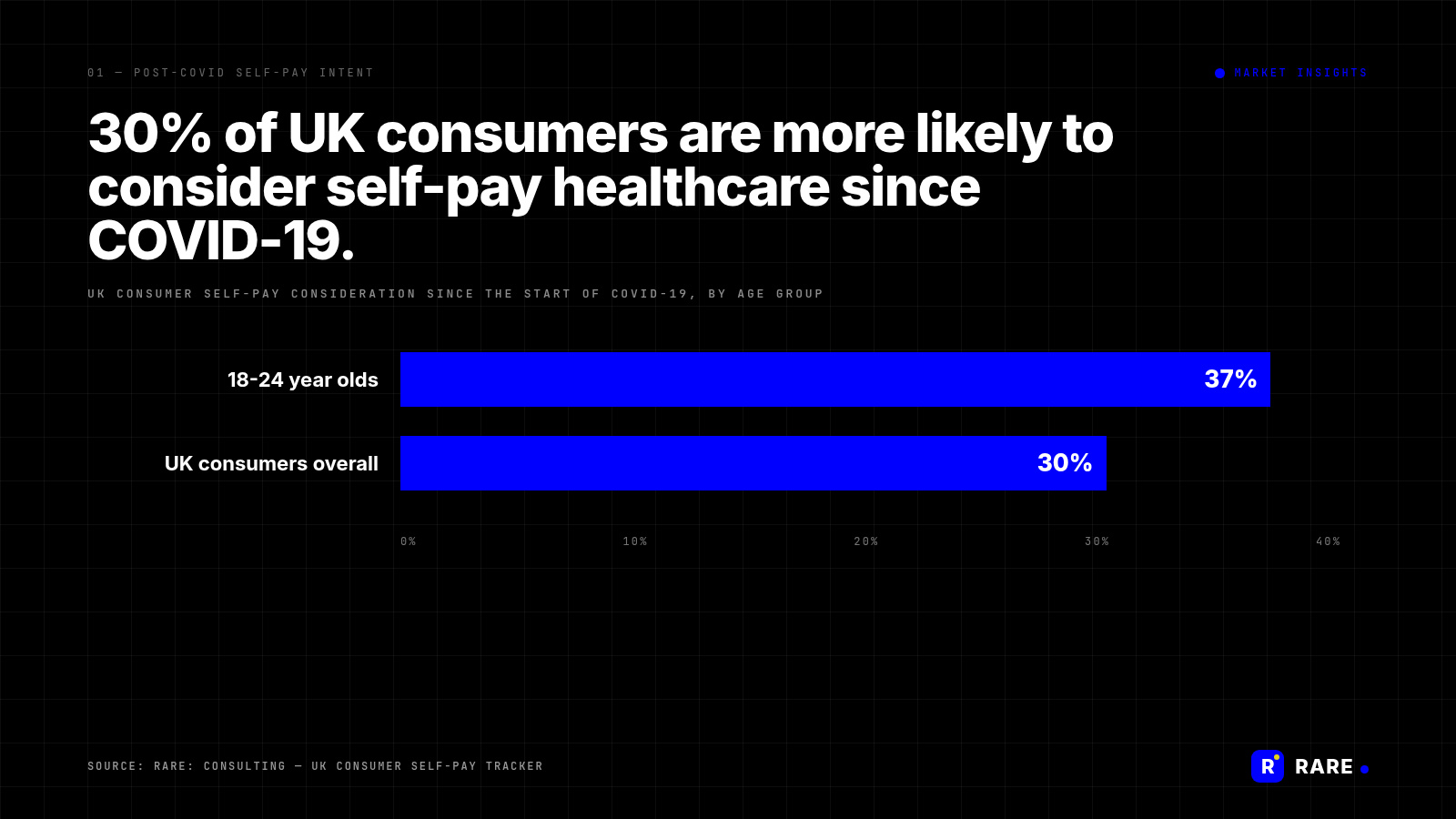

30% of UK consumers are now more likely to consider self-pay healthcare since the start of COVID-19, rising to 37% among 18-24 year olds, according to Rare. tracking. The pandemic compressed years of consumer behaviour change into months. NHS waiting lists swelled, elective procedures fell sharply, and the consumer cohort turning to private healthcare for the first time skewed younger and more digitally comfortable than the historical self-pay base.

How big is the NHS backlog COVID-19 created?

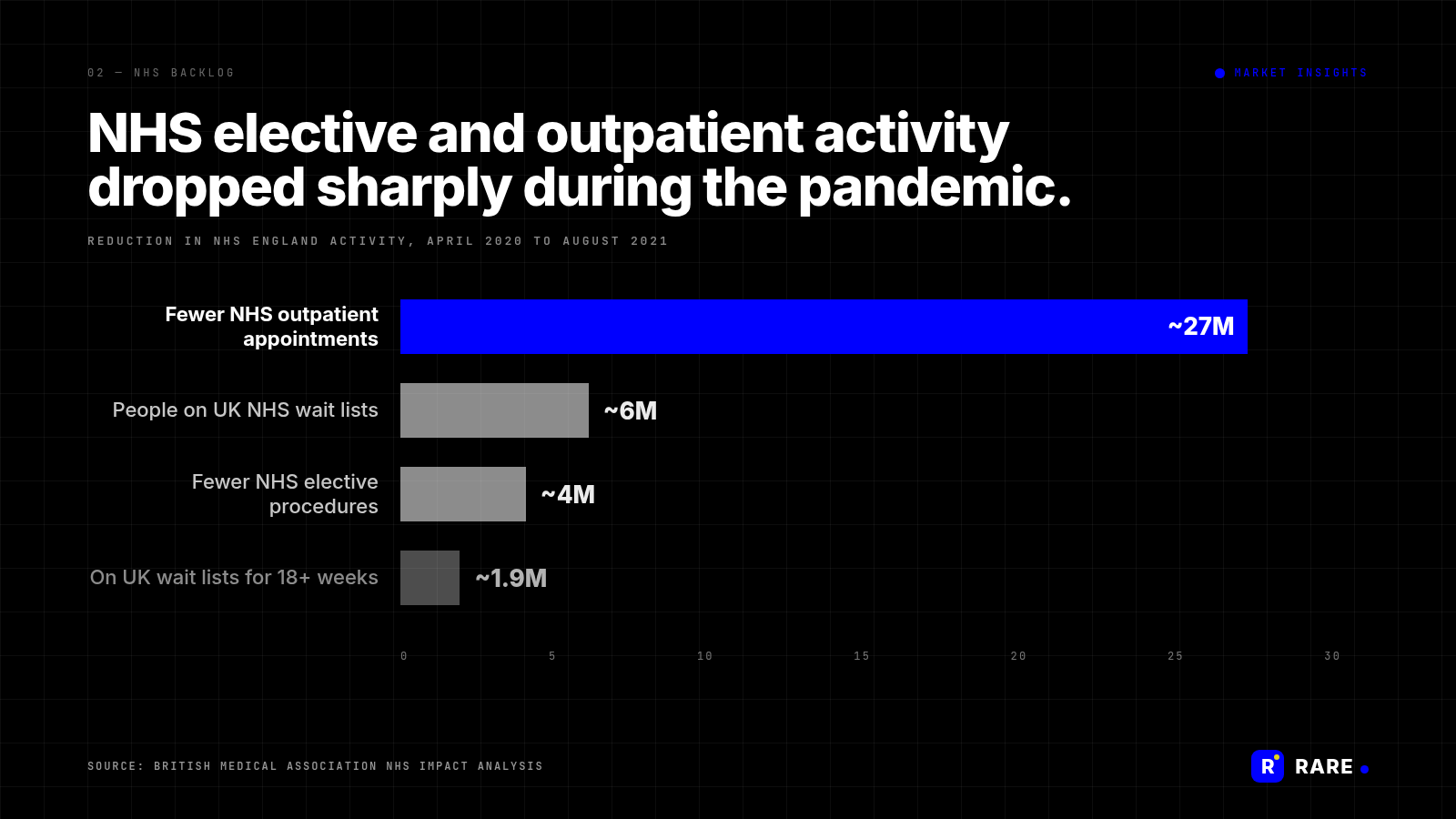

The scale of the NHS backlog is the underlying driver. According to the British Medical Association, between April 2020 and August 2021 there were nearly 4 million fewer NHS elective procedures and roughly 27 million fewer outpatient appointments compared with normal pre-pandemic activity. The BMA estimates that around 6 million people are now on UK NHS waiting lists, of which 1.9 million have been waiting more than 18 weeks.

Those numbers represent unmet healthcare demand that does not disappear. It either gets absorbed back through the NHS over years, or it migrates to private providers in the meantime. The data suggests that a meaningful share is migrating.

How are private institutions easing the strain on the NHS?

Several private healthcare hospitals took on NHS patients during the pandemic to ease the burden on public services. Endoscopy units, oncology services and diagnostic capacity were partially routed through private hospitals where capacity allowed. Others have absorbed self-pay patients seeking private routes to the same treatments because they were unwilling to wait.

The London Clinic, for example, has reported a particular rise in self-pay cancer diagnostic patients. The driver, in their experience, is patients seeking faster access combined with confidence in the safety protocols private institutions established during the pandemic.

Who is the post-COVID UK self-pay patient?

The historic self-pay patient profile was older and more affluent. The post-COVID self-pay patient profile is broader, and notably younger. 30% of all UK consumers report they are more likely to consider self-pay healthcare since the start of COVID-19. Among 18-24 year olds, that share rises to 37%.

The age skew matters commercially. Younger patients are at the start of long healthcare relationships, not the end. Private providers that capture self-pay business from this cohort during NHS waiting-list pressure are likely to retain them as customers far longer than the historic self-pay business model assumed.

The signal sitting underneath the data is generational. The 25-year-old who turned private during the pandemic for a cancer diagnostic, or a physiotherapy referral, or a mental health consultation, is unlikely to revert to a 26-week NHS wait at 35. Lina Patel at The London Clinic puts it plainly: patients are not willing to put their lives on hold. The UK private healthcare base is being reset by a one-off behavioural shift COVID accelerated, and the providers reading the data correctly are not running a tactical backlog play. They are acquiring customers who will use them for thirty years.