In this blog, we explore the latest trends in diversification, within the UK Medical Aesthetics market.

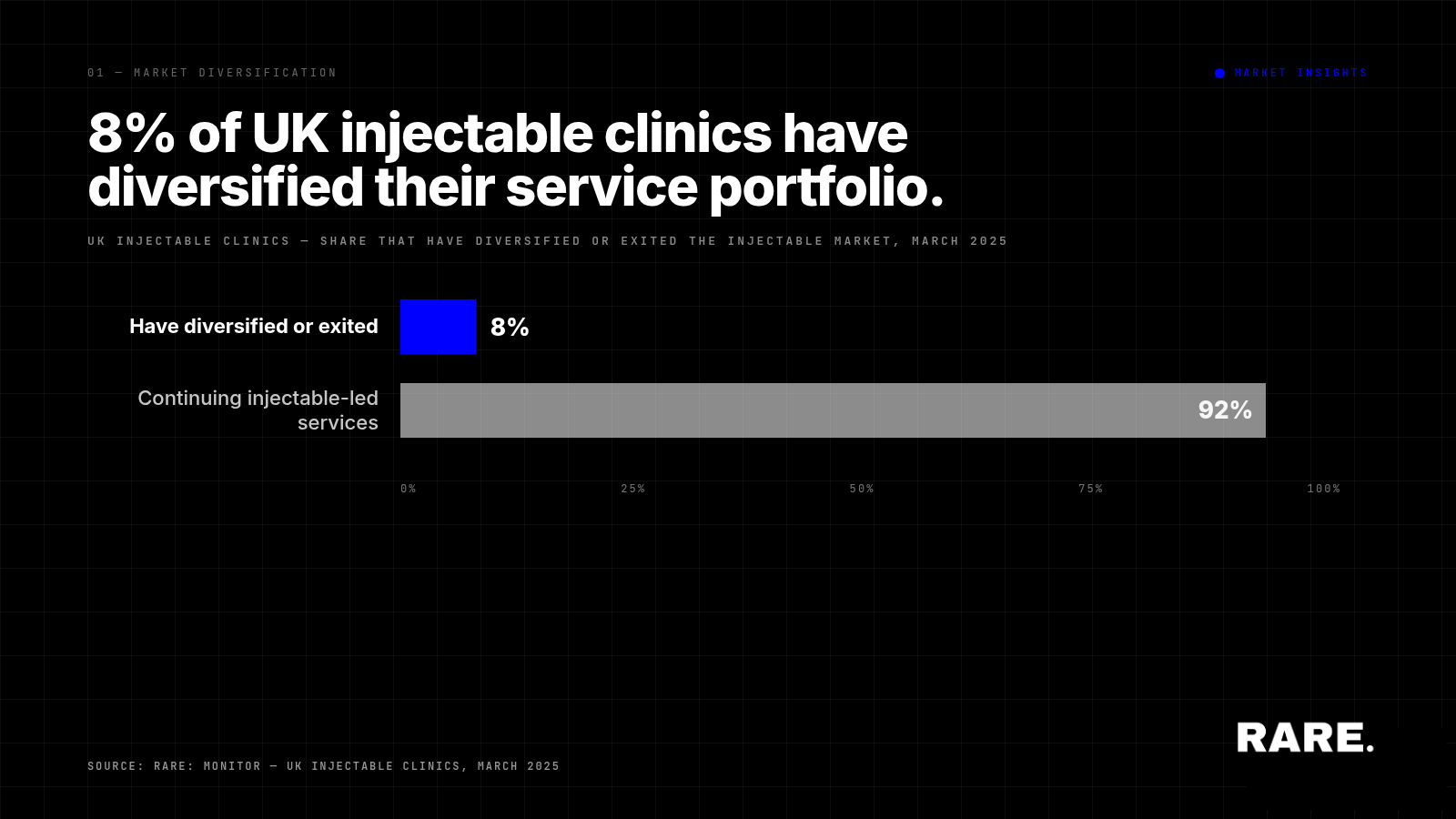

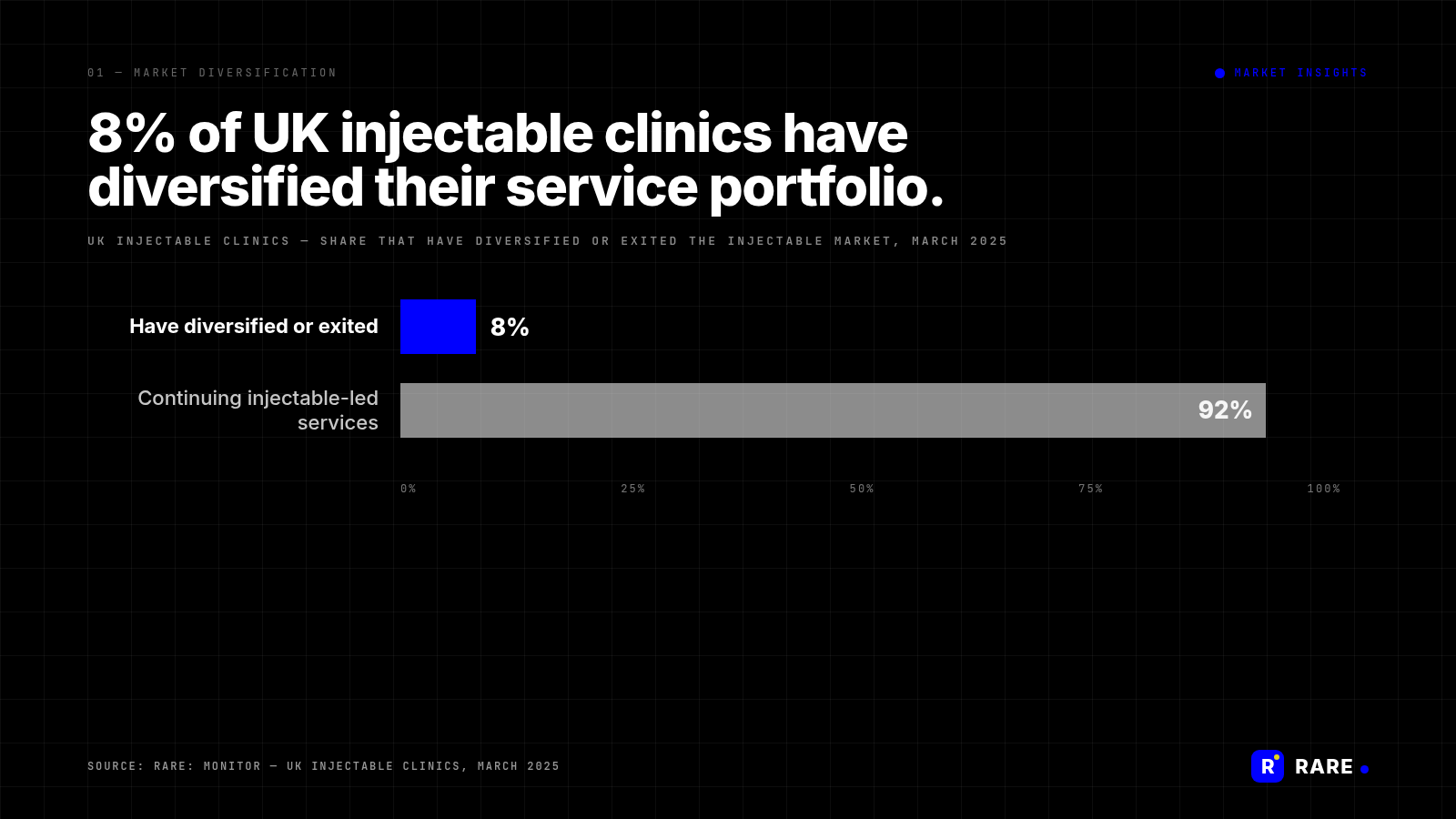

8% of UK injectable clinics have already diversified beyond core injectable treatments or exited the injectable market entirely, according to Rare.Monitor data presented at the ACE Conference in March 2025. Consumer consideration for traditional injectables has fallen sharply, regulatory pressure is tightening on unregulated providers, and a parallel growth of energy-based devices and medical wellness offerings is reshaping what UK aesthetic clinics actually deliver. The category is in active reconfiguration.

How much of the UK aesthetics market has already diversified?

8% of UK injectable clinics have either expanded their service portfolio beyond traditional injectables (typically into medical devices, regenerative treatments or medical wellness) or exited the injectable market entirely. The remaining 92% continue to operate primarily injectable-led services.

8% in a six-to-twelve month window is a meaningful pace of category change. The signal is clear enough that manufacturers, distributors and operators across UK aesthetics need to plan for an addressable market structure that will look measurably different by the end of 2025.

Why is the UK aesthetics market diversifying now?

Three forces are converging.

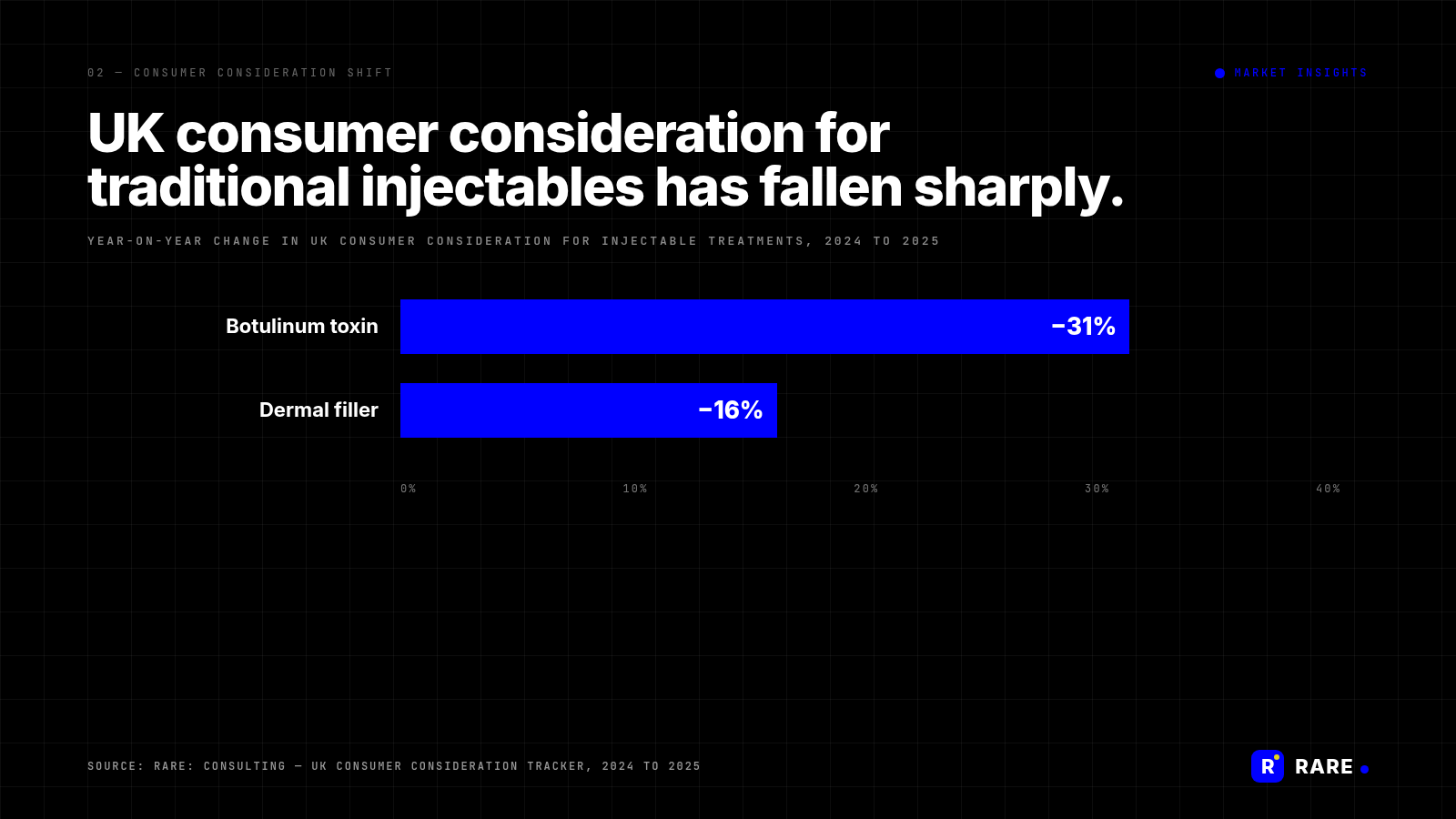

First, consumer consideration is shifting. UK consumer consideration for traditional injectables has fallen sharply year-on-year. Botulinum toxin consideration is down 31%. Dermal filler consideration is down 16%. The drop is large enough that injectable-led commercial models can no longer assume the underlying demand curve.

Second, the medical wellness category is filling some of that demand gap. Around 34% of UK aesthetic providers now offer medical wellness and longevity treatments, in line with growing consumer interest in holistic, long-term health rather than purely cosmetic outcomes. Patients who would historically have considered injectables now have credible alternative options inside the same clinic.

Third, the cost of adding non-injectable devices has fallen. In just the last six months, dermal filler clinics offering non-injectable device-based treatments have grown by 12%. New device manufacturers entering the market, lease-based equipment models and improved training pathways have all reduced the barrier to entry. Clinics can now expand into device-based services in months rather than years.

How is regulation accelerating the shift?

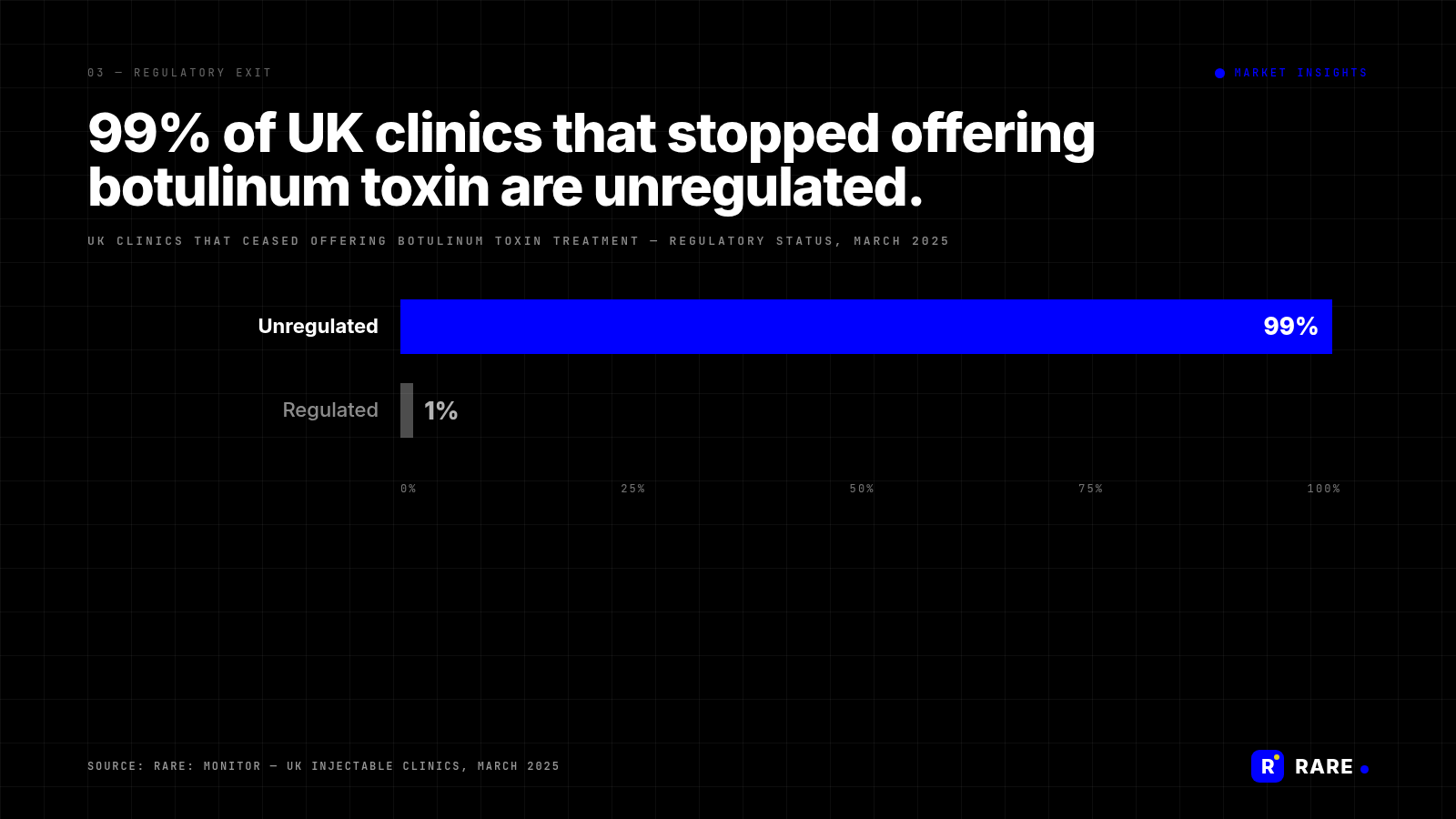

Regulatory pressure is the structural driver underneath the consumer and capability shifts. Of the 6% of UK providers that have stopped offering botulinum toxin, 99% are unregulated practitioners.

This is the cleanest signal in the data. Increasing regulatory oversight is driving unregulated injectable providers out of the market. Some are exiting altogether. Some are pivoting into non-injectable services that carry less regulatory risk. Either way, the regulated providers that remain operate in a quieter competitive landscape, and the bar to entry for new injectable providers has risen sharply.

Regulation is doing what marketing could not. Ninety-nine percent of UK clinics that have stopped offering botulinum toxin are unregulated. Whatever consumer education, KOL endorsement and clinical-quality narrative the regulated incumbents have run for the last decade, regulatory framework changes are filtering the unregulated cohort out of the injectable market faster.

That changes the next twelve months for regulated incumbents. Competitive pressure from unregulated clinics is being removed from the market by something other than commercial competition, and the resulting space is unusual. The brands that move now to lock in clinic relationships, build out distribution agreements, and grow share among the regulated cohort, will inherit a UK injectable market with measurably fewer competitors than they had a year ago. That window does not stay open indefinitely. New unregulated entrants will appear, and consumer-facing brand competition will sharpen again. But for the next twelve months, the regulatory dynamic is doing the work of three years of competitive marketing.

For wider context on the UK aesthetics commercial reset, see the companion analysis: Why licensing regulation will reshape the aesthetics commercial model.

Source: Rare.Monitor, March 2025.